Newsletter Mercados

July 17, 2026 • 776 words • 0 sources

Listen to this newsletter as a podcast

Three voices, natural conversation. Listen while you catch up.

Global Context

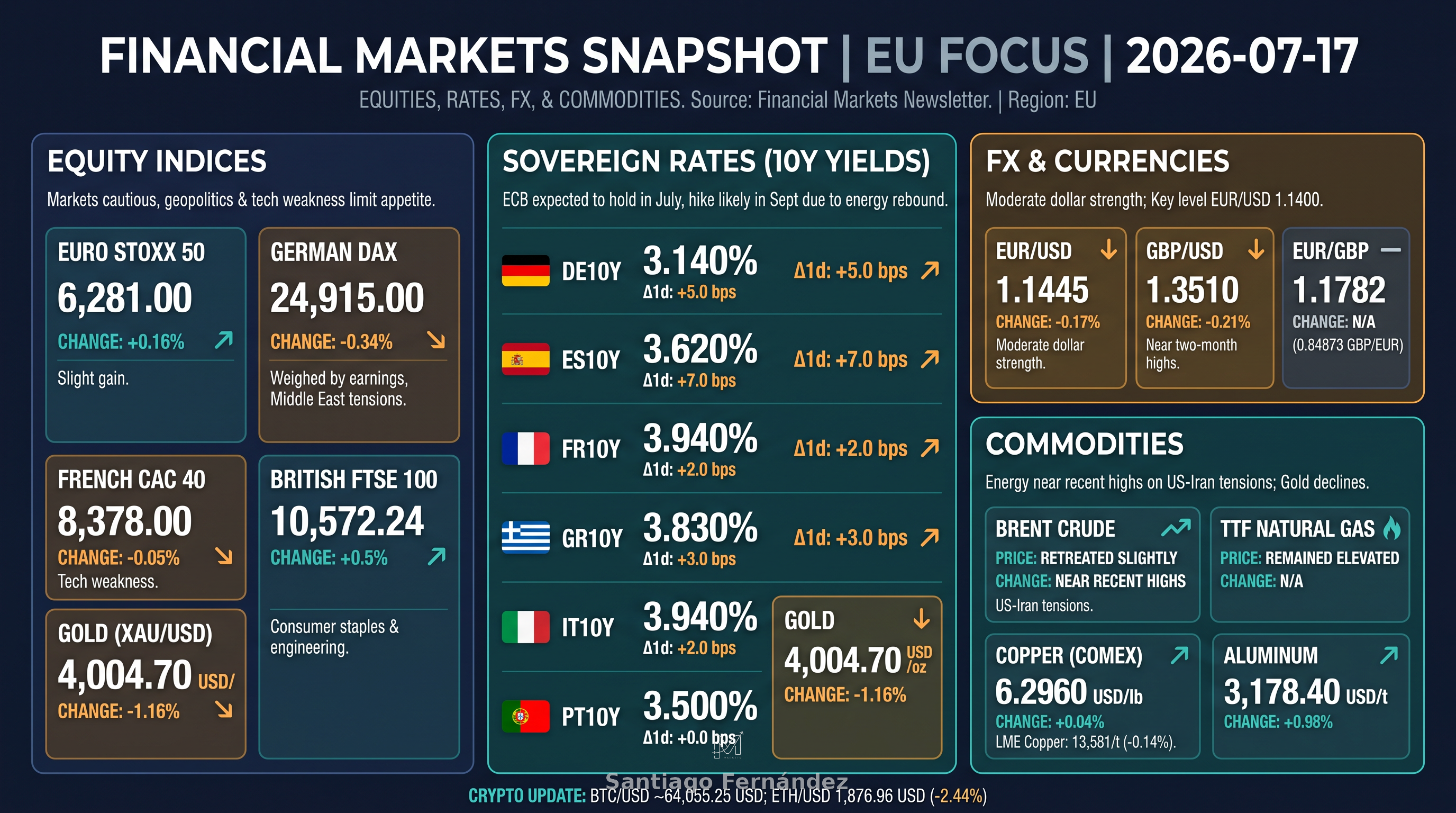

The session on Thursday, July 16, showed widespread caution in European markets, with mixed movements in equities. Geopolitical tension between the U.S. and Iran remains a dominant factor, along with expectations regarding ECB monetary policy. The semiconductor sector showed strength thanks to AI investments, partially offsetting inflationary pressures from energy.

Interest Rates

Specific closing data was not available for European sovereign bond yields (Bund, OAT, BTP, Bonos, Gilts) or for 2s10s/5s30s curves. EUR IRS 10y and USD IRS 10y swaps were also not available. The ECB is expected to maintain rates at its July 23 meeting, although a growing majority anticipates a hike in September.

Sovereign Debt

No closing data was found for sovereign debt spreads (BTP-Bund, Bonos-Bund, OAT-Bund) nor auction results for July 16, 2026.

Corporate Credit

European corporate credit sentiment remained prudent, with geopolitical tensions limiting risk appetite. Neither iTraxx index data nor credit ETF flows (HYG, LQD) were available for the session.

Foreign Exchange

EUR/USD declined 0.17% to 1.1445, reflecting moderate dollar strength. GBP/USD fell 0.21% to 1.3510, though near two-month highs. EUR/GBP stood at 1.1782 (0.84873 GBP/EUR). No data was found for USD/JPY or DXY.

Commodities

Brent crude retreated slightly, but remained near recent highs on US-Iran tensions. TTF natural gas remained elevated. Gold (XAU/USD) fell 1.16% to USD 4,004.70/oz. Comex copper rose 0.04% to USD 6.2960/lb, while LME copper declined 0.14% to USD 13,581/t. Aluminum rose 0.98% to USD 3,178.40/t.

Equities

The Euro Stoxx 50 closed with a slight gain of 0.16% to 6,281.00 points. The German DAX fell 0.34% to 24,915.00 points, weighed down by corporate earnings revisions and tensions in the Middle East. The French CAC 40 declined 0.05% to 8,378.00 points, impacted by tech weakness (STMicroelectronics -4.9%). The British FTSE 100 rose 0.5% to 10,572.24 points, driven by consumer staples and engineering stocks. No data was available for the IBEX 35.

Cryptocurrencies

Bitcoin (BTC/USD) traded around 64,055.25 USD, with a market capitalization of 1.33 trillion USD. Ethereum (ETH/USD) closed at 1,876.96 USD, a 2.44% drop from the previous close, with a capitalization of 233 billion USD.

Conclusion

European markets remain cautious, with geopolitics and energy as the main risk factors. The strength of the dollar and tech weakness limit risk appetite. Attention is expected to focus on the ECB meeting on July 23 and the evolution of tensions in the Middle East. Key levels to monitor include 6,200 in the Euro Stoxx 50 and 1.1400 in EUR/USD.